Decarbonise for net zero

Alice Roberts, Kris Russell

December 19, 2025

Regulatory roundup - Updates on California's Climate Disclosure Law

Our experts discuss a series of changes related to California's Climate Disclosure Law.

Legal update - Temporary SB 261 freeze, no delay for SB 253

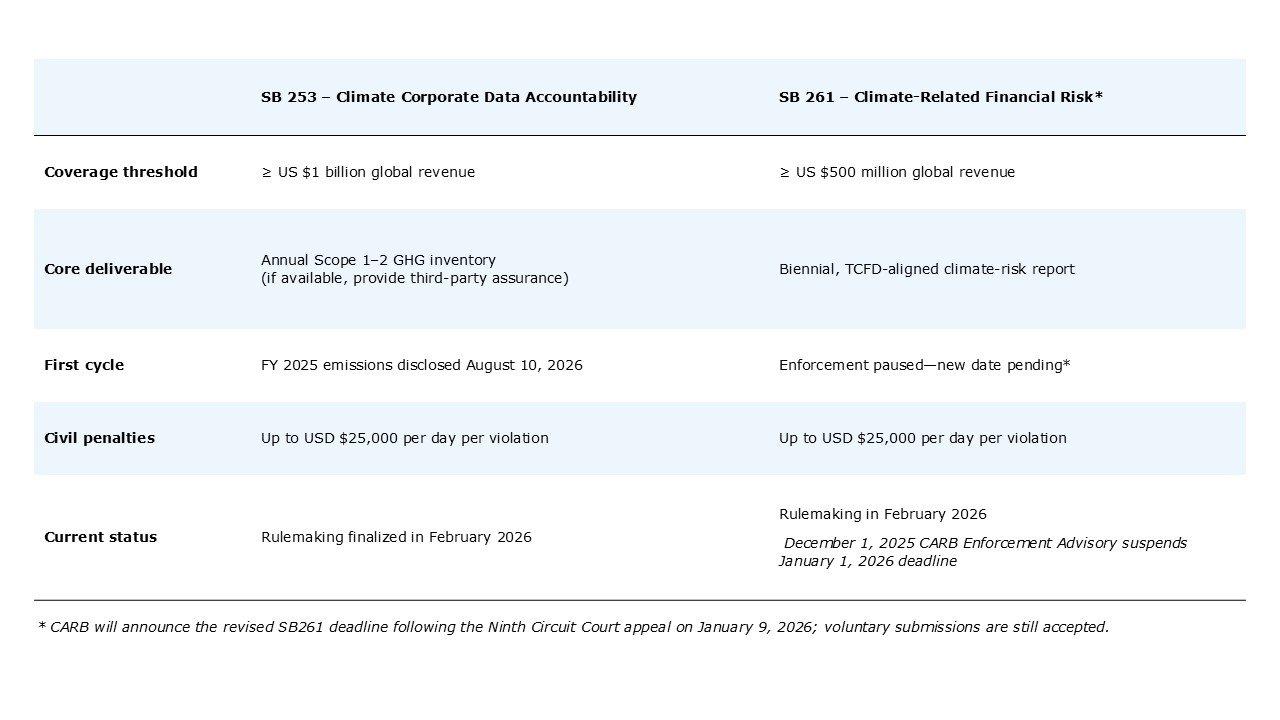

In a significant development for companies subject to California’s new climate disclosure requirements, the US Court of Appeals for the Ninth Circuit issued a partial injunction on November 18, 2025, temporarily halting enforcement of the Climate-Related Financial Risk Act (SB 261). Although the court’s order is formally limited to only the plaintiffs in the suit, the California Air Resources Board (CARB) announced on Dec 1, that it will not enforce SB 261’s January 1, 2026 deadline and will release a new disclosure date, pending the outcome of the appeal. A hearing is scheduled for Jan 9, 2026.

The injunction arises from litigation brought by the US Chamber of Commerce and other business groups, who argue that both SB 253 and SB 261 violate the First Amendment by compelling public disclosures of greenhouse gas emissions and climate-related financial risks. The district court denied injunctive relief in August 2025, prompting the appeal. The stay affects SB 261’s January 1, 2026 reporting deadline, while the court simultaneously declined to pause SB 253, which remains in effect and continues toward an updated August 10, 2026 filing deadline for scope 1 and 2 emissions reporting. The Ninth Circuit issued a partial injunction.

CARB Nov 18, 2025 workshop - Key takeaways

At the November 18 CARB workshop, staff provided additional clarity on the proposed implementation of California’s climate disclosure laws, while underscoring that several elements remain subject to ongoing rulemaking. CARB proposed an August 10, 2026 deadline for initial scope 1 and scope 2 emissions reporting under SB 253, with no assurance requirement for the first reporting cycle in 2026. A limited assurance requirement would begin in 2027 (based on 2026 data). Additional detail on recurring reporting timelines, templates, assurance processes, and enforcement provisions is expected as CARB finalizes regulations, currently anticipated in February 2026.

CARB also clarified how reporting years are determined based on fiscal year-end timing. Companies with fiscal years ending between January 1 and February 1, 2026 will report emissions for the fiscal year ending in 2026, while companies with fiscal years ending between February 2 and December 31, 2026 will report emissions for the fiscal year ending in 2025. All entities will have at least six months after the end of their fiscal year to submit reports. Covered entities will receive a fee notice by September 10 and will have 60 days to submit payment. Notably, CARB has removed payroll and property thresholds from applicability determinations, and revenue applicability will be based on the lesser of the two prior fiscal years. CARB also confirmed that a parent company may submit a single consolidated report on behalf of its subsidiaries if information is combined at the parent level, otherwise subsidiaries must file separately.

For SB 261, CARB indicated that existing climate risk reports aligned with TCFD or ISSB may satisfy requirements, provided they are submitted through the public docket and include appropriate “comply-or-explain” statements.

Dec 1, 2025 update – Enforcement advisory notice

On December 1, CARB issued an Enforcement Advisory Notice that it will not enforce SB 261’s January 1, 2026 deadline and will release a new disclosure date, pending the outcome of the appeal.

CARB also opened a voluntary docket for SB 261 disclosures, allowing companies to voluntarily submit climate risk reports during the enforcement pause.

CARB reiterated that SB 253 is not subject to the injunction and remains fully in effect. CARB also reaffirmed that the first SB 253 reporting year will include meaningful enforcement flexibility. Under CARB’s Enforcement Notice, companies are expected to provide “what they have on hand,” with emphasis on good-faith effort in the first year (including available assurance reports).

Dec 9, 2025 update – Draft regulations issued

On December 9, CARB released draft implementing regulations for SB 253 and SB 261 and announced a public hearing to consider adopting regulations on February 26, 2026. The 45 day public comment period will start Dec 26, 2025 and end February 9, 2026.

Implications for SB 253

CARB has structured the first SB 253 reporting year as a transitional period, exercising enforcement discretion and prioritizing good-faith efforts over complete or fully assured datasets. However, this flexibility should not be misinterpreted as a signal to deprioritize preparation.

The 2026 submission will establish the baseline for all future reporting. Poor GHG boundary decisions, inconsistent methodologies, or weak audit-trail introduced in year one may create future year complications or require restatement once assurance requirements apply. SB 253 ultimately requires full scope 1, scope 2, and scope 3 emissions reporting, with assurance and expanded disclosure requirements beginning in 2027.

California climate reporting at-a-glance

Recommendations for clients

Given the regulatory direction outlined by CARB and remaining areas of uncertainty, we recommend a “no regrets” approach that focuses on actions that will remain valuable regardless of final rule details.

This includes making an early decision to comply, strengthening emissions data, clarifying organizational boundaries, and building governance and documentation practices that support future assurance.

We recommend the following near-term actions.

- Establish governance. Form a cross-functional disclosure task force to coordinate emissions data, climate risk narrative development, internal controls, and assurance readiness.

- Continue preparing for SB 253 without interruption. Initiate 2025 scope 1 and 2 emissions data collection aligned with GHG Protocol standards and review CARB’s draft reporting template to identify gaps.

- Advance SB 261 report. Draft an initial climate-risk narrative aligned with SB 261 disclosure frameworks such as TCFD or ISSB and consider voluntary submission through CARB’s public docket.

- Plan for assurance. Engage assurance providers early to understand expectations ahead of the 2027 limited assurance requirement.

- Assess internal readiness. Maintain core milestones, ensure coordination across sustainability, finance, risk, and legal teams to meet compliance obligations once litigation is resolved. Use this opportunity to strengthen internal controls and improve data quality before enforcement begins.

- Engage in the regulatory process. Review CARB’s draft regulations and prepare comments during the public comment period ending February 9, 2026.

By advancing these activities now, companies can mitigate regulatory risk, establish credible baselines, and position themselves for efficient reporting regardless of how the legal or regulatory landscape evolves. CARB’s workshops, draft FAQs and reporting templates, enforcement discretion, and issuance of draft regulations collectively signal that the intent of SB 253 and SB 261 is active implementation, with preparation and good-faith reporting beginning in 2026. While first-year flexibility is anticipated, it is designed to support good-faith implementation rather than delay. Demonstrating progress toward disclosures that align with the direction and purpose of the laws will be an important signal of readiness and credibility to both regulators and stakeholders.

Get in touch

Alice Roberts

Senior Managing Consultant, GHG Emissions Lead

Kris Russell

Sr Managing Consultant